RIG Update #5 — Huddle and ship

Issuance curve discussions, rainbow staking, committee-enforced inclusion sets, the cost of permissionless liquidity provision, Internet of agents, and more...

Welcome back to Robust communications, your newsletter for all updates from the Robust Incentives Group!

We’ve been staying put, Q1 is always lighter conference-wise, but that doesn’t mean we’ve been at rest, far from it. We have so many updates we’re excited to tell you about, so let’s dive in.

📝 Issuance curve: A proposal and an endgame

Caspar and Ansgar (EF Consensus R&D) released two notes on reviewing the issuance curve in light of long-term sustainability.

The first post, “Electra: Issuance curve adjustment proposal” describes features of an issuance curve designed by Anders in his previous issuance curve research (also discussed in our Update #4).

We argue why under the current issuance policy, in the long run most ETH will plausibly be staked via LSTs.

High staking ratios have negative externalities:

LSTs are a winner-takes-most market due to network effects of money. This LST could replace ETH as the de facto money of Ethereum. But for true economic scalability, the money of Ethereum should be maximally trustless: raw ETH.

Economies of scale and network effects induce more demand for LSTs as the staking ratio increases, making solo stakers relatively less competitive.

ETH holders are diluted beyond what is necessary for security.

We briefly introduce the endgame vision for staking economics: a stake targeting policy. However, we also highlight remaining open questions which make it not viable for Electra.

We thus suggest adjusting the issuance curve in Electra as per Anders’ proposal. It is trivial to implement, but significantly reduces the incentive for new stake inflow and helps to mitigate many of the issues outlined above.

The second post, “Endgame Staking Economics: A Case for Targeting”, reviews arguments for a stricter issuance curve, opinionated about maintaining the staking ratio (amount of ETH staked divided by total supply of ETH) in a certain range.

Today, 30M ETH or 1/4 of all ETH, is staked, with the trend of increasing staking showing no signs of stopping.

We argue that most of new stake will be driven by LSTs, which gain in money-ness with adoption and time.

A world in which most of ETH is staked through LSTs has several implications that we consider negative: LSTs have winner-takes-most dynamics due to network effects of liquidity. Economies of scale increase competitive pressure for solo staking viability. Further, a LST replacing ETH as the de facto money of the network (apart from L1 tx fees) leads to Ethereum users being exposed to counterparty risk inherited by the LST by default. For true economic scalability the money of Ethereum should be maximally trustless.

Today, the issuance yield does not ensure a limit to the amount that can be staked profitably. LSTs have significantly changed the cost structure of staking, making it possible that most ETH will be staked eventually.

We argue that endgame staking economics should include an issuance policy that targets a range of staking ratios instead, i.e. around 1/4 of all ETH. The intention is to be secure enough but avoid overpaying for security and thereby enabling said negative externalities.

Finally, we highlight some open research questions that need answering to make a targeting policy feasible.

The two posts have fostered an active discussion on “whether” and “how” to adjust the issuance curve with a view towards long-term sustainability of Ethereum network economics. This discussion is expected to continue for the foreseeable future, with further research initiatives addressing several related questions. You can also catch Caspar and Ansgar on Jon Charbonneau and Hasu’s podcast, Uncommon Core 2.0.

📝 Rainbow staking 🌈

In the meantime, Barnabé continues his quest to unbundle everything everywhere all at once, with “Unbundling staking: Towards rainbow staking”. This time, the lens is on staking, reframing the role of validators as providing a suite of protocol services, which may be decoupled from one another and re-assigned to operators optimally suited for each specific service.

We take a first principles approach to identifying the services that the Ethereum protocol intends to provide, as well as the economic attributes of various classes of service providers (e.g., professional operators vs solo stakers).

Heavy and light categories of services: We re-establish the separation between heavy (slashable) and light (non- or partially slashable) services. Accordingly, we essentially unbundle the roles that service providers may play with regard to the protocol. This allows for differentiated classes of service providers to be maximally effective in each service category, instead of lumping all under a single umbrella of expectations, asking everything of everyone.

Intended goals: We believe the framework of rainbow staking helps to achieve several goals:

The correct interface to integrate further “protocol services” in a plug-and-play manner.

Targeting Minimum Viable Issuance (MVI) and countering the emergence of a dominant LST replacing ETH as money of the Ethereum network.

Bolstering the economic value and agency of solo stakers by offering competitive participation in differentiated categories of services.

Clearing a path to move towards SSF with good trade-offs.

📝 The more, the less censored: Introducing committee-enforced inclusion sets (COMIS) on Ethereum

A new post by Thomas, Francesco (EF Consensus R&D) and Barnabé introducing a new design for committee-based inclusion lists inspired by Multiplicity (see also the current ROP-9).

Today, a majority of builders and relays censor Ethereum transactions interacting with sanctioned addresses. Advancements in protocol research have led to new designs and specifications for single-proposer inclusion lists, allowing for the improvement of the network’s censorship resistance properties by enabling proposers to force the inclusion of transactions in subsequent blocks. However, relying on a single entity to construct inclusion lists introduces potential vulnerabilities to commitment attacks.

In this post, we introduce committee-enforced inclusion sets (COMIS): A candidate implementation of a multiplicity gadget on Ethereum, which assigns the construction of an inclusion set to a committee composed of multiple parties, rather than a single proposer. We examine the feasibility of implementing COMIS considering the following properties: Inclusion guarantees, accountability, robustness to commitment attacks, consensus load and overall complexity.

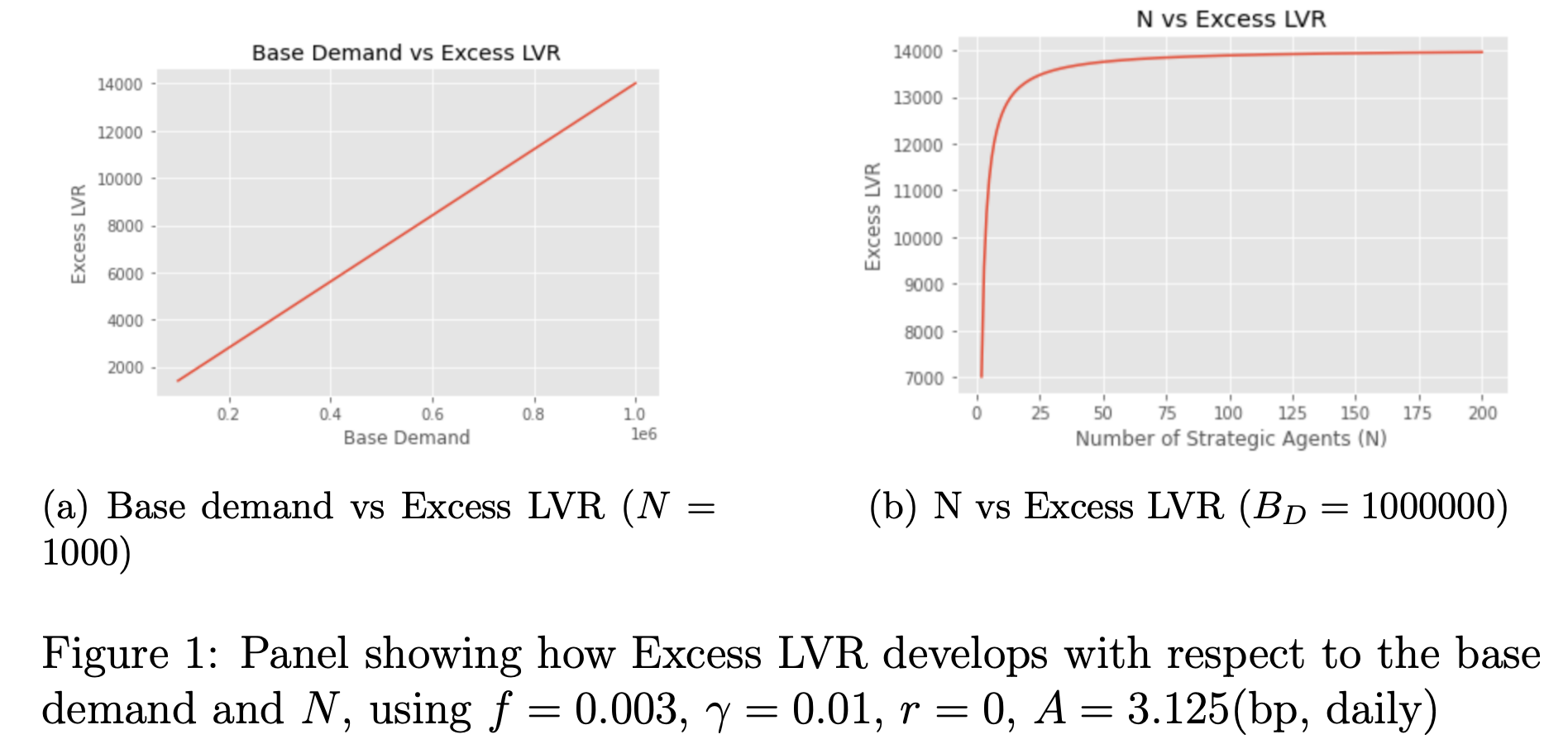

📜 The Cost of Permissionless Liquidity Provision in Automated Market Makers

Julian published his first paper (woop woop!), “The Cost of Permissionless Liquidity Provision in Automated Market Makers” along with Davide.

Automated market makers (AMMs) allocate fee revenue proportional to the amount of liquidity investors deposit. In this paper, we study the economic consequences of the competition between passive liquidity providers (LPs) caused by this allocation rule. We employ a game-theoretic model in which N strategic agents optimally provide liquidity. In this setting, we find that competition drives LPs to provide excess liquidity. In the limit, the excess liquidity converges to a constant that linearly increases with the amount of base demand, demand that is insensitive to trading costs. Providing excess liquidity is costly as more capital is exposed to adverse selection costs, leading to a loss in welfare. Our main result is that the price of anarchy, defined over the liquidity provider performance, is O(N), implying that the welfare loss scales linearly with the number of liquidity providers. We show that this result is still observable when using richer aggregate demand models.

📝 The Internet of Agents

Davide published “The Internet of Agents”, a foray into the world of Crypto and AI.

In this post, I will make the case that the integration of blockchain infrastructure and AI agents is desirable and that it will give rise to an Internet of Agents:

An upgrade to the current paradigm of interconnectivity, augmented with incentives and modern cryptography, that will allow us to reap the benefits of an economy driven by AI agents with unprecedented levels of security, efficiency, and collaborative potential.

I will then discuss the path to get there. I will focus on short-term use cases and applications, some of which are already being designed and developed. I will discuss their limits and potential improvements, as well as the research needed across AI and blockchain to unlock new use cases in the medium-term.

Davide also participated in the first Open Source AI Summit, organised by Illia Polosukhin and Erica Kang, held at Stanford University.

📝 Reconsidering the market structure of PBS

Barnabé released a new post investigating whether to move forward with ePBS or not, in light of new proposals to enshrine further separation between validators and the block production service.

I believe the implementation of ePBS should be considered holistically, in comparison with other choices such as execution tickets and validator–proposer separation more broadly. ePBS does improve upon certain aspects of the current MEV-Boost market, such as providing access to a trustless path and giving us the ability to enshrine different mechanisms like slot auctions. Yet, ePBS is concerned with the allocation of building rights, primarily, and perhaps this is not a problem the protocol should concern itself with. It may be enough indeed to allocate proposing rights, and relinquish control and observability past that point.

📝 Initial Analysis of Stake Distribution

Rounding out the staking news with a new post by Julian, providing a minimal model to understand the distribution of stake across diverse agents:

Ethereum issues ETH to validators for performing their consensus duties. The amount of issuance depends on the amount of ETH staked. The current issuance curve may result in a very high long-term staking ratio. This post aims to analyze whether a change in the level of issuance, as proposed to be implemented in the next Electra upgrade, affects the distribution of staking mediums investors use. We differentiate between three mediums of staking: 1) investors may solo-stake, 2) investors may deposit their tokens with a decentralized staking service provider (SSP), or 3) investors may deposit their tokens with a centralized SSP. Subsequently, we define the cost structures of each staking medium. Finally, we model a linear programming problem in which an investor decides what fraction of their endowment to hold or stake via which medium based on the expected monetary return and an investor’s non-monetary preference, such as convenience, trust, and decentralization. Our main result is that the distribution of stake does not depend on the level of issuance. We show how the model can be used with two examples.

This post presents a minimum non-trivial model to analyze the distribution of stake with respect to the level of issuance. We refer the reader to this post for an explanation of why a change to the issuance curve may be useful. This post does not aim to discuss the motivation for an issuance reduction, nor does it aim to be maximally precise about the cost structures of different SSPs. What this post does aim to do is to ground the conversation around staking distributions in an addressable manner.

Extra bytes

Anders provided a long-form comment exploring minority discouragement attacks in the context of a staking fee and increased attestation penalties.

It can be clarifying to start by reviewing specific attacks that can be executed when penalties and rewards are tilted to favor some specific consensus role, for example either the attester or proposer. Such attacks can arise or become more severe under a regime of increasing penalties. The reader may also wish to familiarize themselves with the concept of discouragement attacks, although the discussion will be kept at a basic level throughout this comment.

Davide contributed to an analysis of execution tickets by Jonah Burian (Blockchain Capital), focused on pricing.

We present an economic analysis of the Execution Tickets mechanism. We setup a framework that allows us to characterize how the value of Execution Tickets (the assets) changes with different configurations of the allocation and lottery mechanisms. We derive foundational results that have important implications when thinking about the design and the feasibility of such a mechanism for selling the right to propose an execution block in Ethereum. Our goal is to build on these results and implications as we work on validating pricing and allocation mechanism designs.

We’re reading “Anoma as the universal intent machine for Ethereum” by our friend Christopher Goes (Heliax/Anoma).

📖 RIG Open Problem (ROP) updates

Opened and funded ROP-8: Geographical distribution of Ethereum validators.

Opened ROP-9: Multiplicity gadgets for censorship-resistance.

See also COMIS above!

Opened and funded ROP-10: Economic validation of execution tickets.